Productive Parallels: Financial Risk Tolerance

What should your risk tolerance be and how to increase it.

We have all heard the wild stories of the massive risk the most successful businessmen of today took in order to get to where they are. Elon Musk investing nearly all of his PayPal exit into the then not so promising Tesla and SpaceX, Jeff Bezos quitting his high paying wallstreet job to start a book shipping company, or Sara Blakley taking her last $5k in savings and working on development in her basement, even writing her own patent after teaching herself how off of books from Barnes and Noble to eventually becoming the youngest female billionaire off of her product, Spanx. While these are inspiring stories of taking massive risks and betting on oneself, they are not the only examples. Everyone has their story of taking a risk and it paying off. Anything from talking to that guy or girl in the library that later became their spouse, deciding to risk embarrassing themselves when starting a new hobby that turned out to be one of the most enjoyable pastimes they have, or deciding to switch career paths without a guarantee that it will either pay more or lead to a better quality of life. The risks do not have to be massive in order to be important, but oftentimes the larger the risk the larger the payoff. With that understanding, if you believe that you are an incredibly capable agent, then a very large bottleneck for your level of success is your risk tolerance. How much risk are you willing to take on? Many inspirational speakers, self help gurus, and successful entrepreneurs with a podcast will tell you that there is no calculus here, you just need to have an unreasonable amount of self belief and grit in order to have that bet you took out on yourself hit. I think that the world of investing and portfolio management could help us put some numbers to what risk should look like for us individually and take some of the irrational guesswork out of how much we take on. There is a lot of survivorship bias in this advice, for every success there are thousands of failures. And yes, the only way you lose is if you give up and “what’s the alternative” aphorisms are nice but I know a lot of people would feel more comfortable taking those risks if they could put some verifiable frameworks behind it. If you are anything like me loss aversion kicks your ass sometimes and some tools to help combat it would be useful. Welcome back to productive parallels where we look at fields of study and work to glean insights that help you improve your life. We are looking into the world of finance, more specifically risk and how to increase your tolerance and appetite for it.

To figure out your risk tolerance you can use the metrics of willingness and capacity. Willingness is a measure of your psychological ability to handle risk, are you the type to panic sell or more the type to hold until it’s worthless. In other words, how well can you ride the waves of volatility in the market? If willingness is your psychological ability to ride the waves, capacity is your financial ability to weather the storm. Can you afford your lifestyle and overall financial goals if the market has a down year, how liquid do you need to be, how long is your time horizon on withdrawal, ect. It can be explained as the hard constraints, your income, savings, debts, time lines, liquidity ect. These things are far harder to change and even when change does occur it is often downstream from an alteration in mindset around or mental framing of decisions that lead to said changes. With that being said, there are still some useful frameworks that can be used even without direct data.

Capacity

Most of the questions the equations and models that are used when determining capacity aim to answer are A how much do we have to risk, B how much do we stand to gain given the risk, and C how much loss can we withstand. Without getting into the numbers, we can take these questions and the methods used to answer them to establish our baseline for risk. For example, to answer question A we would use our basic financial information like income, debt, and expenses in conjunction with the Kelly criterion. The basic financial info gives us the big picture of our whole pot. The Kelly criterion is used to maximize the long-term compound growth rate of your portfolio while avoiding the risk of losing it all. It does this by figuring out how much of the entire portfolio to allocate to this risk. The Kelly criteria looks like this:

f* = (bp − q) / b

f* i s the fraction of your current bankroll to wager.

p is the probability of winning.

q is the probability of losing (which equals (1 - p).

b is the decimal odds, or the net fractional payout of the bet (e.g., a “2 to 1” payout means you stand to win $2 for every (1 wagered, making b = 2$).

We can use our prior experiences and current research to apply rough estimates of probability to the scenario. This then provides us with a rough number for how much of our time, money, or mental capacity we should be allocating to a particular bet. Even if we don’t implement the numbers here we can still use the general goal of the Kelly criterion as a guideline for decision making. The heuristic would be “how much can I risk without losing it all?”. Oftentimes that number or action is a lot larger than we originally thought. When weighing the options, the riskier one often feels life or death, the Kelly criterion prompts us to think in terms of not best and worst case, but one standard deviation above worst case.

We can answer B, how much do we stand to gain given the risk, by using the Sharpe ratio. The Sharpe ratio measures our return relative to the risk taken. In other words, a ratio of risk to reward.

Sharpe Ratio = (Expected Return − Risk-Free Rate) / Standard Deviation

The expected return is what you would get from taking the risky choice. The risk free rate is just that, risk free. In other words, what your life looks like if everything stays the same. Lastly the standard deviation is accounting for the variance, the range of possibilities between going well and poorly. When calculated it tells you how much “excess return” you get for each unit of volatility. Again even if we did not plug in numbers the general process of getting this ratio can be used to help us make risky decisions. In three quick questions we can come to an answer:

What is the upside if this goes well

What does my life look like if nothing changes

Is the difference between them worth the amount of risk it would take to achieve the desired result from question one.

Lastly question C, how much loss can we withstand? For this we can use a simple coverage ratio. Your liquid assets divided by your monthly expenses. The number you get tells you how long you have before you hit the point of no return. In a more abstract usage this can be seen as your life satisfaction or fulfillment divided by your existential dread or unhappiness. How much longer do you think you can realistically continue living the way you are before you can no longer handle it.

With all three of these questions answered, even if just using the abstracted, decision heuristic versions, provide a concrete framework on which you can feel confident in your level of risk taking.

Willingness

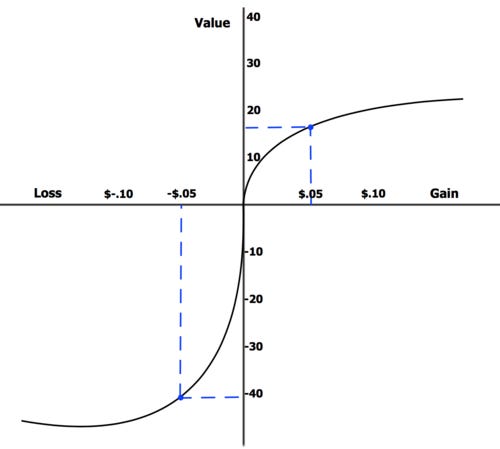

We can look at willingness through the greater lens of prospect theory. If you have read my stuff before you could probably guess who came up with it. Ding, ding, ding, that’s right, Kahneman and Tverskey. Prospect theory was first described in their 1979 paper “Prospect Theory: An Analysis of Decision under Risk,”. It proposes that people are not rational and describes how we make decisions under uncertainty. One of the most well known mechanisms they found is known as loss aversion. They found through many studies that have since been replicated that people weigh the pain of a loss as roughly 2x as painful as the same amount gain is pleasurable. For example if someone lost $100 then the equal amount of pleasure to the level of pain felt would come from a $200 win. This graph illustrates it more cleanly. The value of a five cent gain is half that of a five cent loss.

What this means is that we make many decisions not to win but to avoid losing. Armed with this knowledge we can look at our anxiety or for lack of a better term “icky” feeling around risk as irrational and instead view it through a more objective lens. If we are scared of making that career change or starting that new side hustle, we can discount the negative feelings by 2x. This means that we would need to be more than 2x as anxious or worried as we would need to be certain or excited to go for the risky choice for it to be rational to follow the anxious feelings directions. By asking yourself if your dread is exponentially larger than your excitement for the opportunity you can increase your willingness.

Another way to increase willingness from the financial world is to backstop. This means that you have an emergency fund or some sort of account that is to be left untouched just in case everything goes wrong. The psychological safety net that is created from the knowledge of the financial backstop cand ameliorate some of the excess resistance to willingness. In our own lives this looks like cultivating quality relationships that we know we can rely on, creating quality habits that keep us on track at the very least, and piling a large stack of evidence that we can take risks and both fail and recover as well as succeed. Having the knowledge that we can both rely on ourselves and our network to fix the mess we may end up in makes the risky choice easier to make.

Conclusion

Making risky decisions will never be a comfortable process, by its very nature it is nerve racking, self doubt inducing, and an overall unpleasant experience. By using the frameworks from the financial sector on risk tolerance, specifically capacity and willingness, we can quantify our concerns and make more rational decisions. By using the capacity questions to generate your baseline you then have a ceiling of risk. You will know right off the bat if something is too risky given your current situation. However, that means that everything under it is fair game. This is where the 2x negative feelings heuristic and backstopping should be implemented to try and capture as much of the space between the floor and ceiling as possible. You don’t need to be born a risk taker, it is something that you can work on and become better at using basic math and psychological principles.